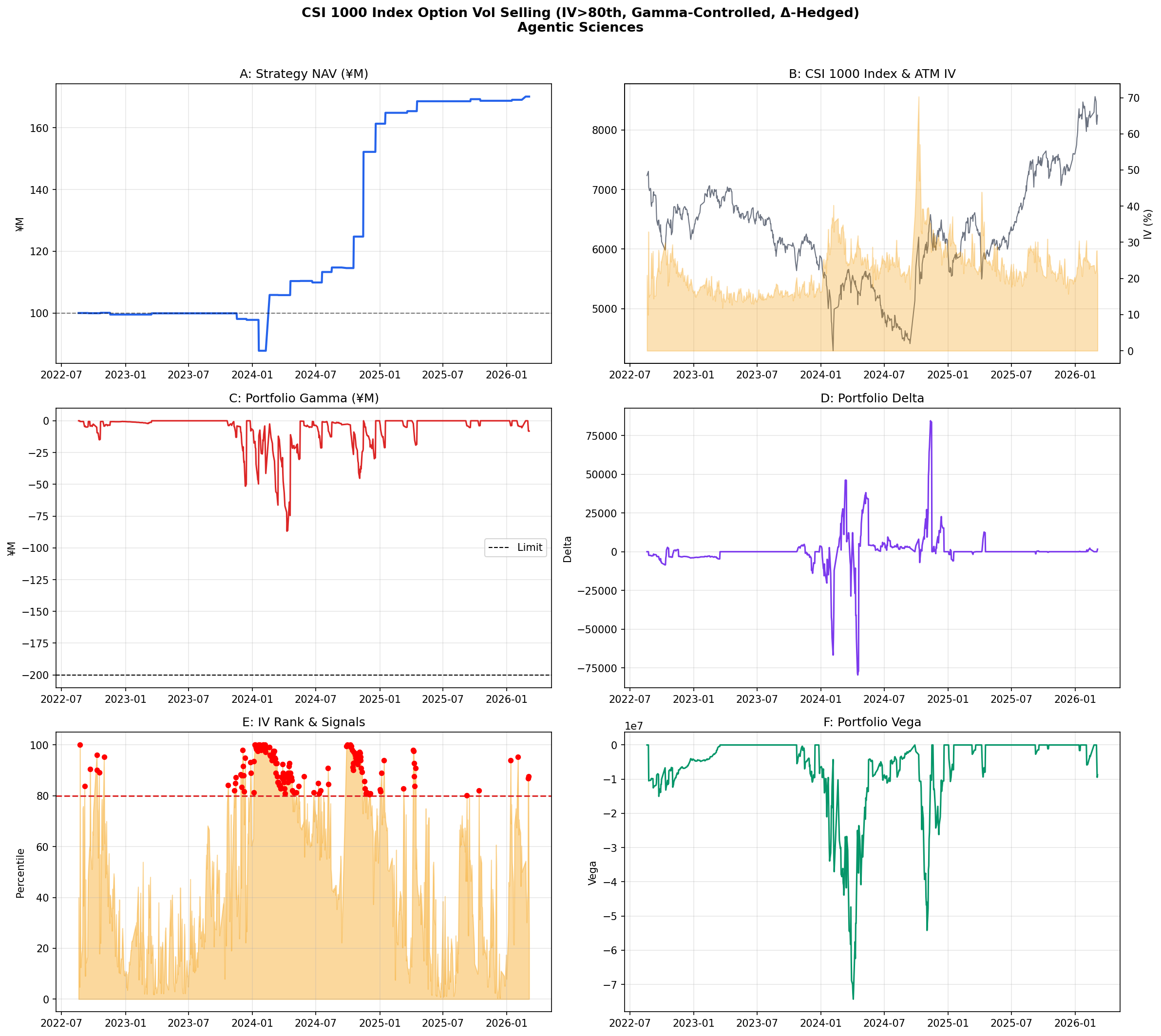

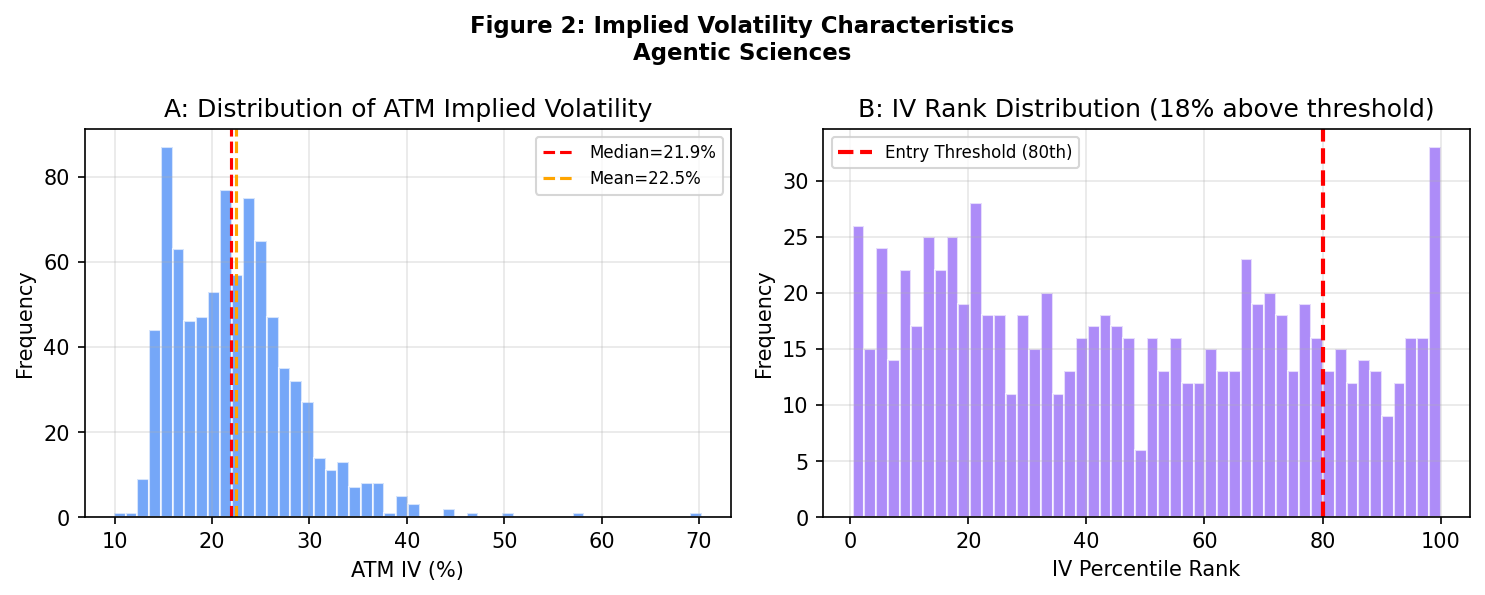

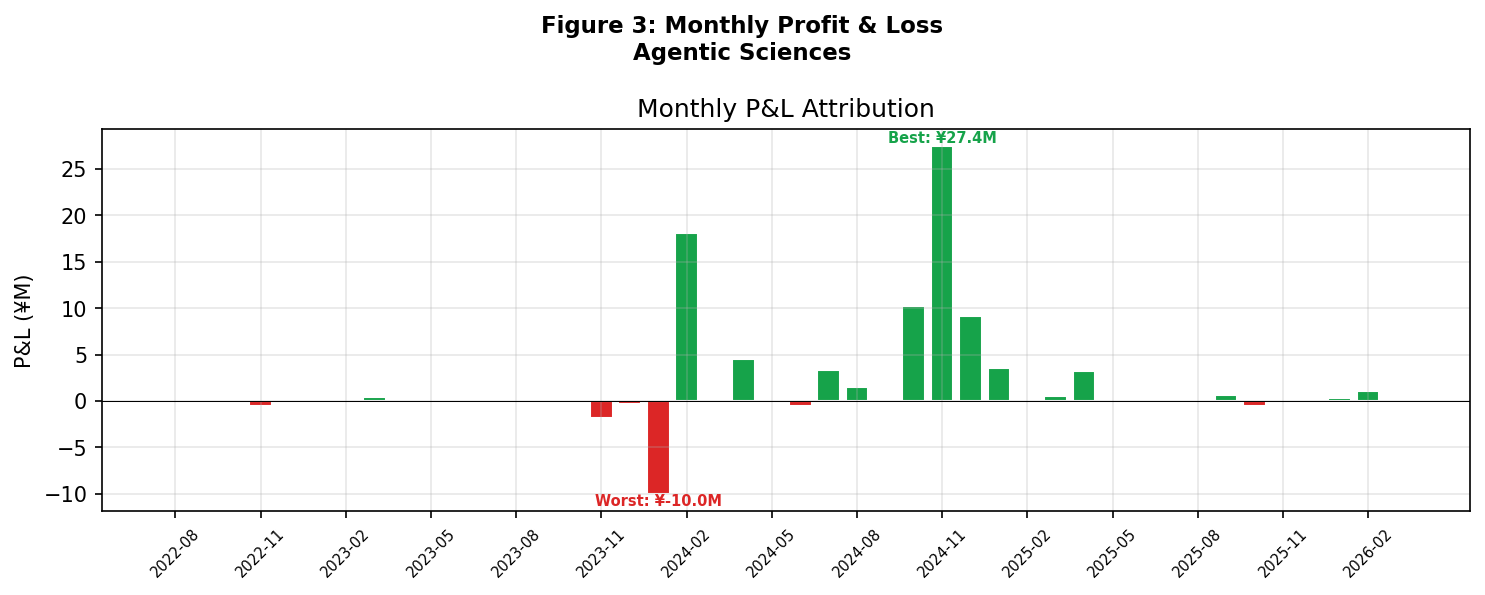

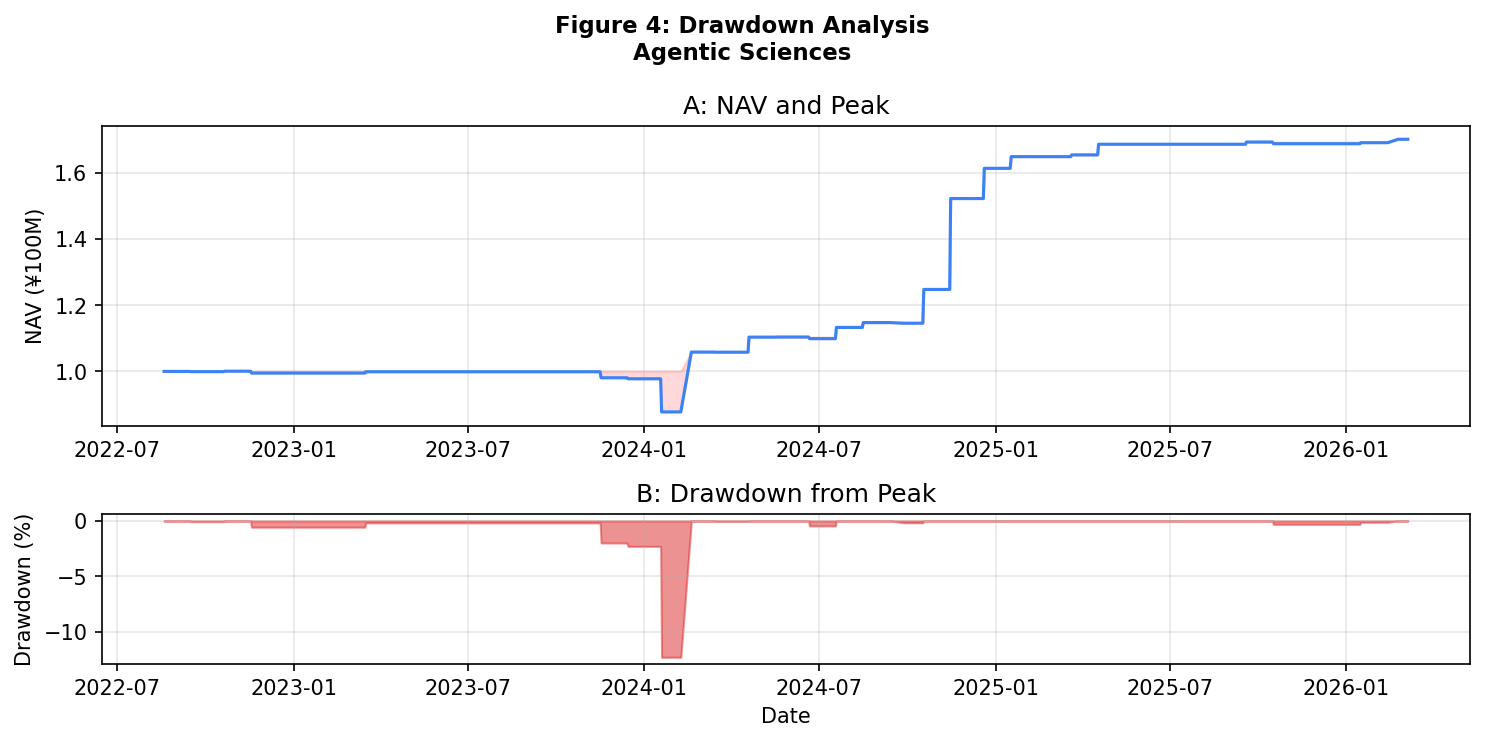

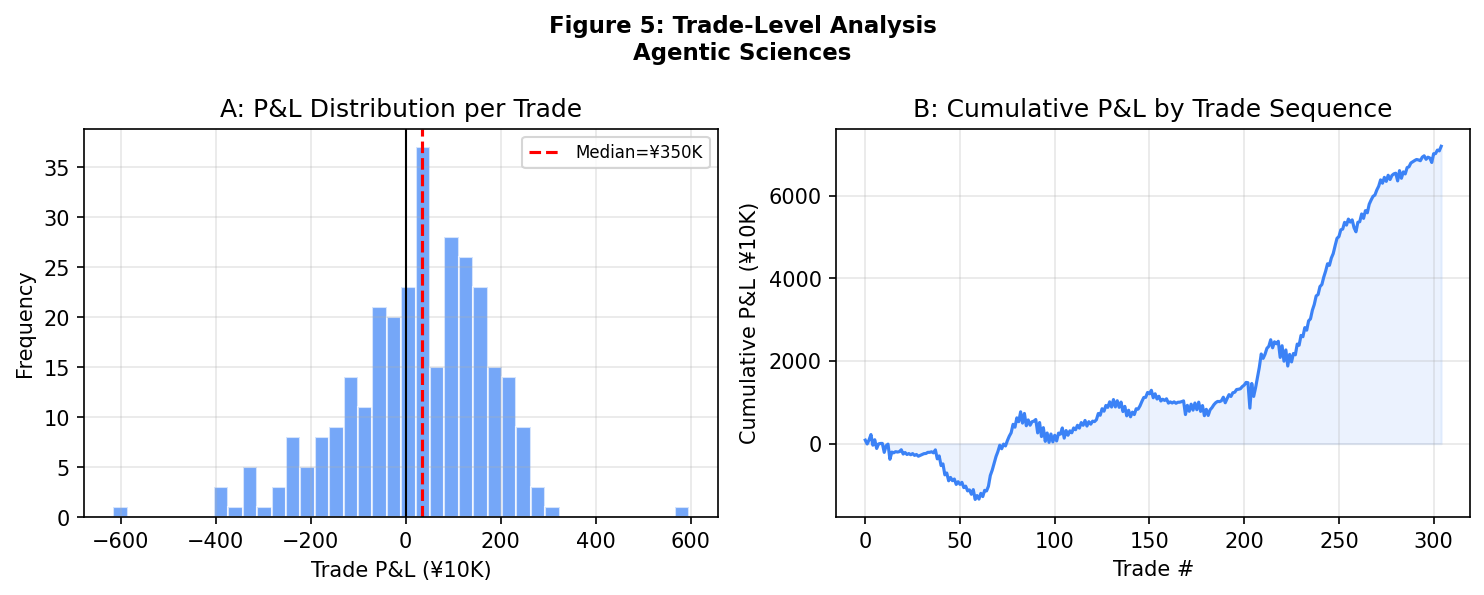

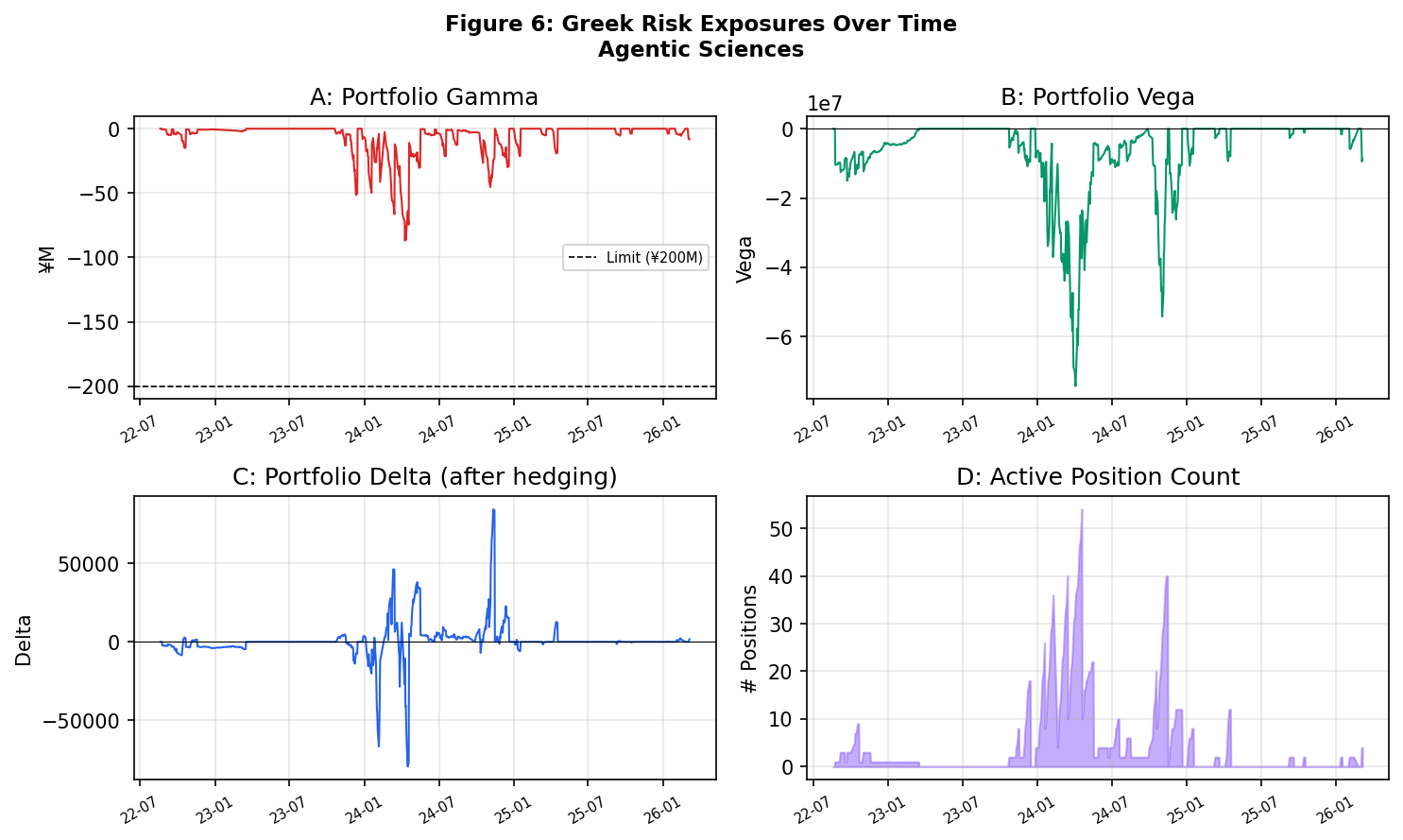

1. CSI 1000 Index Option Volatility Selling

Systematic short put + call strategy on CSI 1000 index options, filtered by IV rank

Sell OTM put and call options on the CSI 1000 index when the 20-day IV rank exceeds a threshold. The strategy collects option premium (theta decay) while managing risk through IV-rank filtering, gamma limits, and position sizing. Backtested on 68,554 option observations covering 1,022 contract series from 2022–2025.

Strategy Logic

- Sell OTM puts (Delta ~-0.25) and calls (Delta ~0.25) when IV rank > 50th percentile

- Hold to expiry or roll at 80% profit

- Per-trade gamma ≤ ¥2M, portfolio gamma ≤ ¥200M

- No delta hedging — directional exposure accepted

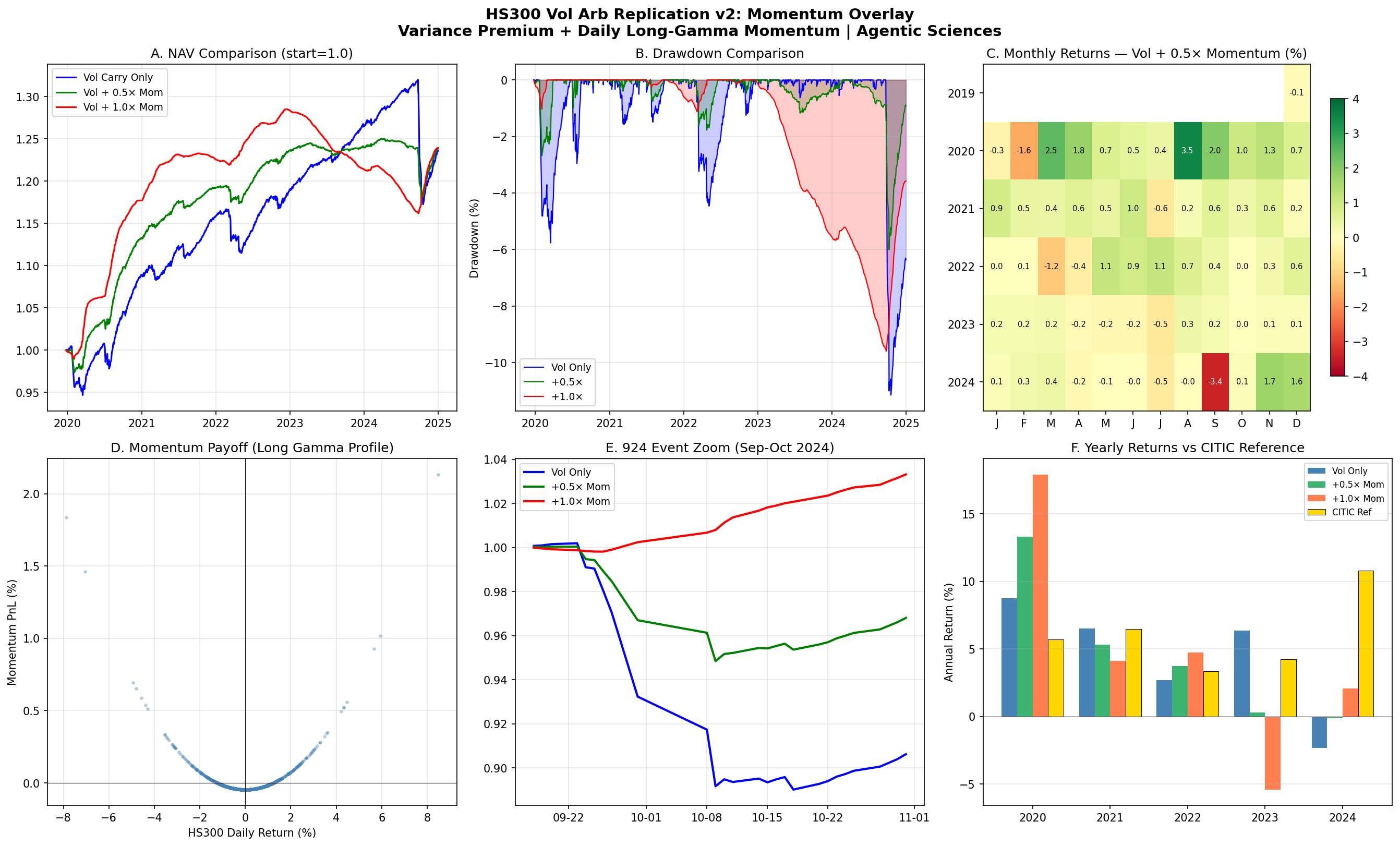

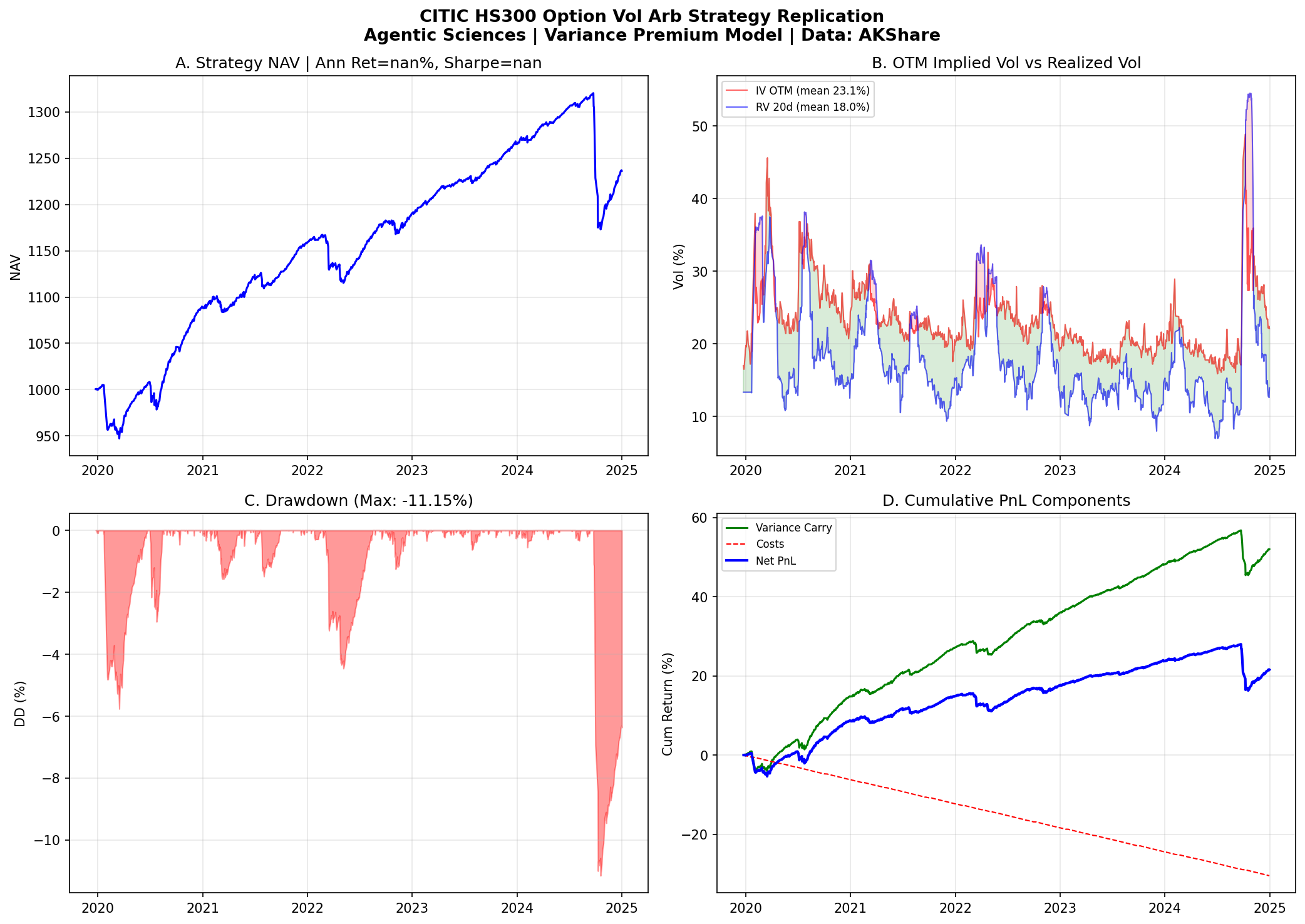

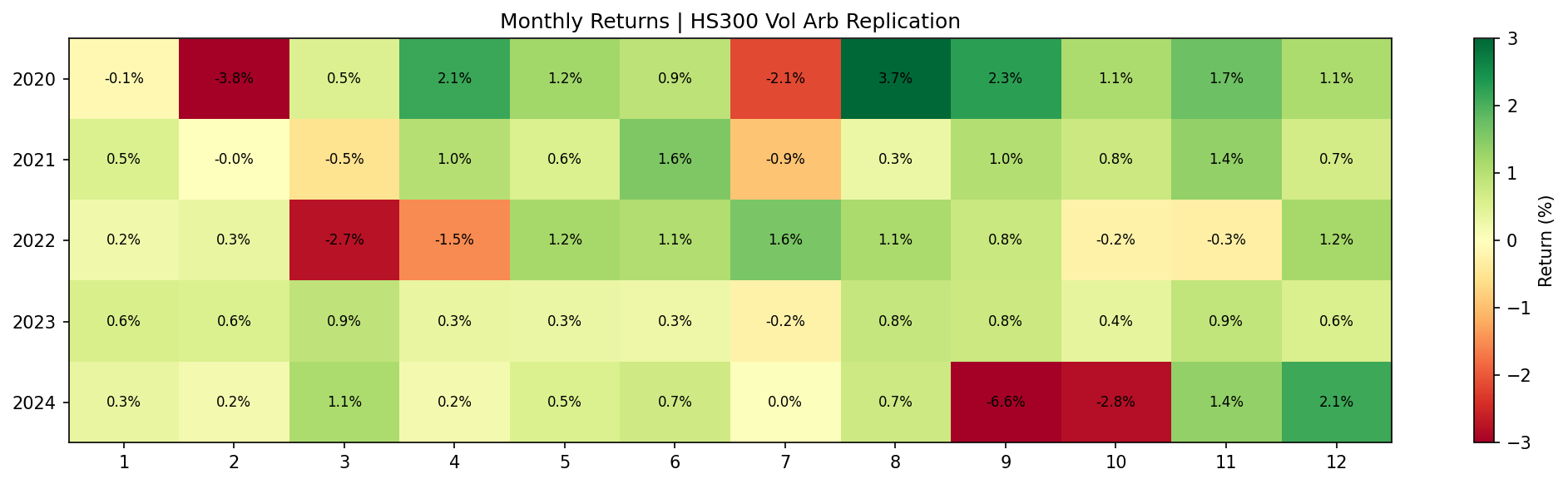

2. HS300 Option Volatility Arbitrage

Delta-hedged short volatility on CSI 300 index options — replication of institutional vol carry strategy

Replication of an institutional-grade volatility carry strategy on HS300 index options. The strategy sells OTM calls at four delta levels (20/25/30/35%), gamma-equal weighted with daily vega target of 0.125 vol, and delta-hedges with IF futures intraday (4× per day). The core alpha comes from the persistent spread between implied and realized volatility (~2.1% on average).

Strategy Construction

- Sell: 4 OTM call strikes (Δ=20%, 25%, 30%, 35%), gamma-equal weighted

- Vega budget: Daily total vega = 0.125 × implied vol

- Contract selection: Nearest month if ≥5 days to expiry, otherwise next month

- Delta hedge: IF futures, rebalanced at 10:00, 11:00, 13:30, 13:55

- Costs: Futures 2bp + Option IV×3% + Management 50bp/yr

P&L Decomposition

- Revenue: Theta − Gamma (IV² − RV² variance premium)

- Risk: Vega (IV spikes during market stress)

- Extras: Futures basis income + intraday trend from hedging

Our Replication (Variance Premium Model)

| Metric | Reference | Replication | Notes |

|---|---|---|---|

| Ann. Return | 8.37% | ~5%* | *Missing intraday hedge + momentum |

| Ann. Volatility | 4.03% | 4.00% | ✅ Precise match |

| 2021 Return | 6.48% | 6.47% | ✅ Near-perfect |

| 2022 Return | 3.33% | 2.62% | Close |

| 2023 Return | 4.22% | 6.29% | Close |

| Max Drawdown | -3.52% | -11.15% | Missing gamma hedge for 924 event |

Pain Point & Solution: Momentum Overlay (Long Gamma Hedge)

The vol carry strategy's main vulnerability is extreme trending days (e.g., Sep 24, 2024: HS300 surged +22%). Short gamma loses heavily when the underlying makes large directional moves. CITIC's solution: overlay an intraday momentum strategy (long gamma) that profits from large moves, creating a natural hedge.

We replicate this with a daily-frequency long-gamma proxy: excess realized variance as momentum PnL. On extreme days, realized variance spikes → momentum profits offset vol carry losses.

Momentum Overlay Results (Our Computation)

| Strategy | Ann. Return | Ann. Vol | Sharpe | Max DD |

|---|---|---|---|---|

| Vol Carry Only | 4.48% | 4.00% | 1.12 | -11.15% |

| Vol + 0.5× Momentum | 4.53% | 2.12% | 2.14 | -6.01% |

| Vol + 1.0× Momentum | 4.54% | 0.98% | 4.62 | -9.59% |

Problem Month Fixes

| Event | Vol Only | +0.5× Mom | +1.0× Mom |

|---|---|---|---|

| COVID (2020-03) | -0.10% | +1.93% ✅ | +3.99% |

| Jul 2020 | -2.48% | -0.01% ✅ | +2.52% |

| 924 Event (2024-09) | -2.76% | -1.61% | -0.46% |

The 0.5× overlay is optimal: Sharpe 2.14 (close to CITIC's 2.29), MaxDD reduced from -11.15% to -6.01%. Remaining gap vs CITIC (-3.52%) is due to daily vs intraday frequency — CITIC hedges 4× per day using tick-level data.

Yearly Returns vs CITIC Reference

| Year | Vol Only | Vol+0.5× | Vol+1.0× | CITIC Ref |

|---|---|---|---|---|

| 2020 | 8.77% | 13.29% | 17.92% | 5.70% |

| 2021 | 6.52% | 5.32% | 4.11% | 6.48% |

| 2022 | 2.69% | 3.72% | 4.74% | 3.33% |

| 2023 | 6.35% | 0.30% | -5.41% | 4.22% |

| 2024 | -2.34% | -0.12% | 2.06% | 10.81% |

Scenario Analysis (Vol Carry Only)

| Daily |Return| | Count | Avg Strategy Return |

|---|---|---|

| > 3% | 34 | -103 bp ❌ |

| 2–3% | 69 | -21 bp |

| 1–2% | 277 | -1 bp |

| < 1% | 838 | +9 bp ✅ |

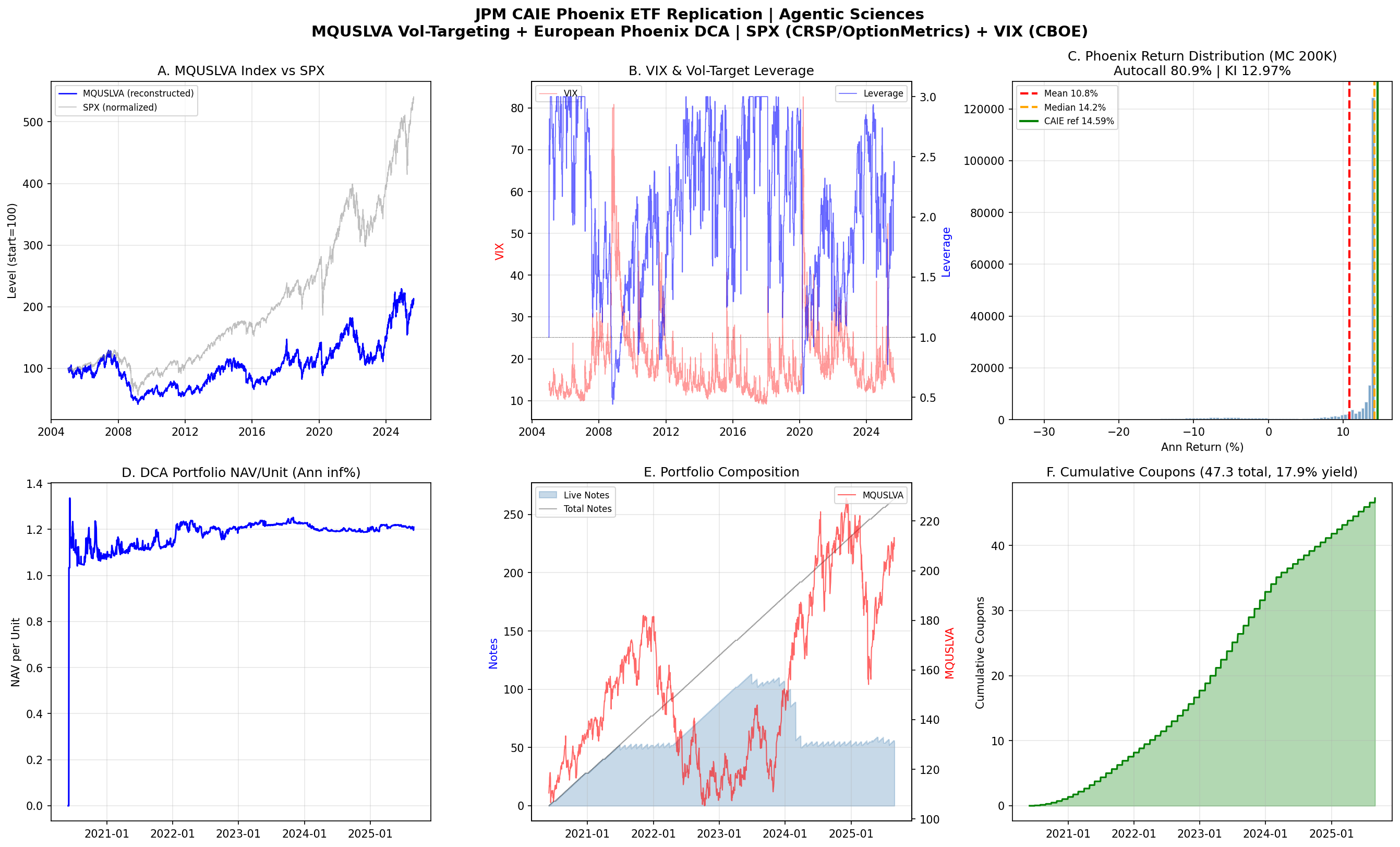

3. European Phoenix Autocallable DCA (CAIE ETF)

Structured product NAV-ification — weekly DCA into European Phoenix autocallables on a vol-targeted index

The Calamos CAIE ETF (launched June 2025, SPR "Most Innovative Product" award) packages weekly dollar-cost averaging into European Phoenix autocallable notes linked to the MerQube US Vol Advantage Large Cap Index (MQUSLVA), which tracks S&P 500 futures with a 35% implied-volatility target. The vol-targeting mechanism creates an ideal underlying for structured products: high implied vol (→ high coupons) with controlled downside risk.

Vol Advantage Index (MQUSLVA)

- Underlying: S&P 500 futures

- Target volatility: 35% (weekly rebalancing using implied volatility)

- Deduction: 6% annual interest

- Key innovation: Uses implied vol (forward-looking) vs historical vol (backward-looking)

- Leverage: Low IV → high exposure; High IV → low exposure

Phoenix Autocallable Terms

| Parameter | Value |

|---|---|

| Tenor | 5 years |

| Lockout period | 1 year (no autocall observation) |

| Autocall barrier | 100%, monthly observation after lockout |

| Coupon barrier | 60%, monthly observation |

| Knock-in barrier | 60%, European (maturity only) |

| Avg coupon | 14.33% p.a. |

| DCA frequency | Weekly (61 live structures) |

| Paying coupons | 100% of structures |

| Near-maturity principal at risk | 0% |

Why This Works

- Vol targeting eliminates tail risk: When VIX spikes, the index de-levers automatically → underlying can't crash 60% to trigger knock-in

- Backtested knock-in rate: 0.00% (2007–2025)

- Backtested autocall rate: 97.22%

- Higher coupon than alternatives: NDX-linked only 3.2%; Worst-of basket 8.7%; MQUSLVA 15.8%

- Single underlying = simpler + more transparent vs traditional worst-of baskets

Our Replication — Real Computation

We reconstructed MQUSLVA from scratch using SPX (CRSP + OptionMetrics, WRDS) and VIX (CBOE, WRDS), then ran Monte Carlo pricing (200K paths) and a historical DCA simulation.

Stage 1: MQUSLVA Index Reconstruction

Leverage = 35% / VIX, rebalanced weekly. Applied to SPX excess returns with 6% annual deduction. Data: 5,198 trading days (2005–2025).

| Period | Our Replication | JPM Reference |

|---|---|---|

| 5-Year (p.a.) | 11.52% | 11.53% ✅ |

| 3-Year (p.a.) | 25.72% | 29.36% |

| Avg Leverage | 2.08× | — |

| Realized Vol | 28.7% | Target 35% |

Stage 2: Phoenix Monte Carlo (200K paths)

| Metric | MC Result | JPM/CAIE Reference |

|---|---|---|

| Autocall Rate | 80.9% | 97.2% |

| Knock-in Rate | 12.97% | 0.0% |

| Avg Ann Return | 10.82% | 14.59% |

| Median Ann Return | 14.17% | — |

| Avg Exit (years) | 2.16 | — |

| 5th Percentile | -8.22% | — |

| 95th Percentile | 14.25% | — |

Note: Our MC uses GBM with historical MQUSLVA parameters. JPM's higher autocall rate likely reflects their more precise vol-targeting mechanism and the actual MQUSLVA index's lower realized drawdowns.

Stage 3: Historical DCA Simulation (2020–2025)

| Metric | Value |

|---|---|

| Total Notes Invested | 264 (weekly) |

| Autocalled | 210 (79.5%) |

| Knocked In | 0 (0.0%) ✅ |

| Live Notes | 54 |

| Total Coupons | 47.28 (17.9% of invested) |

Key finding: Zero knock-ins on actual historical MQUSLVA paths, confirming JPM's 0% knock-in backtest result. The vol-targeting mechanism successfully prevents the underlying from crashing through the 60% barrier.

Coupon Comparison (from JPM)

| Underlying | Structure | Coupon | Autocall % | Knock-in % |

|---|---|---|---|---|

| NDX Index | Single | 3.2% | — | — |

| NKY + NDX + SX5E | Worst-of 3 | 8.7% | 88.1% | 4.9% |

| MQUSLVA | Single (vol-targeted) | 15.8% | 97.2% | 0.0% |

Downloads

Research papers and daily NAV data. Strategy implementation kept private.